Around 30 years ago, the wiring in a car added up to a few hundred meters in length. However, if we were to measure the cumulated length of the electrical wiring in a car today, it would come out to be around 3-4 km. This is so because cars today are not merely a means of transport but a blend of mobility and comfort. One of the most critical but often overlooked elements that make this comfort possible is the wires and cables that work behind the scenes, connecting and powering various electrical systems and components – everything from lighting and infotainment systems to critical safety features.

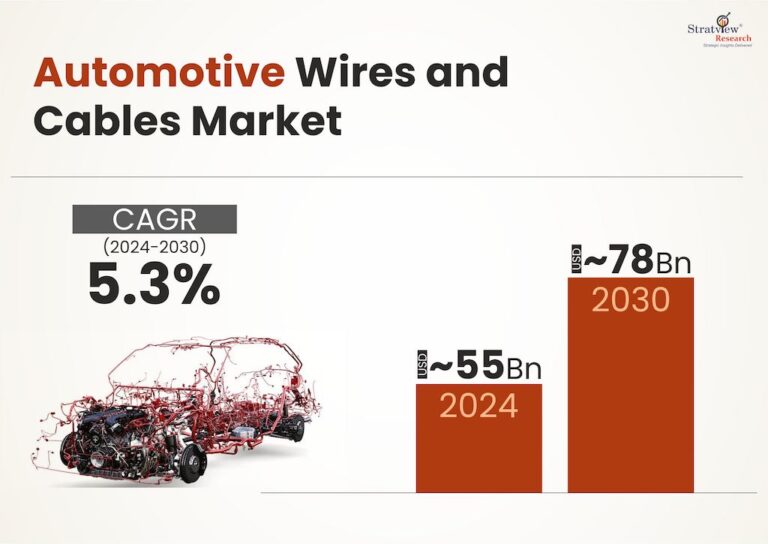

The global automotive wires and cables market stood at a whopping USD 55 billion in 2024. In this article, we’ll explore the various factors shaping this market.

What’s Powering the Market:

The industry is not merely evolving but accelerating towards a future defined by electrification and automation. Manual handbrakes are transitioning to electronic parking brakes, autonomous parking systems are replacing old-school parking sensors, hydraulic tailgates are shifting to electric tailgates, and more. For instance, Advanced Driver Assistance Systems (ADAS), which were once exclusive to luxury vehicles, are now found in over 90% of cars sold in the US, each equipped with at least one ADAS feature. With the increasing integration of such electronic systems to support new-gen vehicles, the demand for automotive wires and cables is surging.

Additionally, with the advent of modern features, new categories of wires and cables find their way onto the wheels. Ethernet cables, once leveraged only to feed internet to our computers and WiFi routers, are now also found in high-end cars to enable high-speed data transfer in systems like driver assistance, infotainment, security and more. For the same applications, OEMs also install Optical Fibre cables (Mercedes Benz), Coaxial Cables (Audi) and Shielded Twisted Pair (STP) cables (Tesla). As the industry moves forward, mass-market brands are expected to incorporate these cables in their vehicles, opening up new possibilities.

Furthermore, the global push towards electric powertrains is expected to be a major driver as well. Currently, internal combustion engine (ICE) vehicles account for over 50% of the global wire harness usage, mainly due to their large fleet size and increasing connectivity and electronic features. The wires most required in ICE vehicles are low-voltage (LV) types, functioning at 12V or 48V, which supply power to crucial systems such as lighting, infotainment, safety, and climate control. As ICE vehicles operate with 12V batteries and alternators producing up to 14.5V, LV wiring does the job for ICE vehicles. However, the rise of hybrid and electric vehicles (EVs) is driving demand for high-voltage (HV) wiring capable of handling 200V to 800V (the operational battery voltage in EVs). Moreover, EVs are far more complex than ICE vehicles, requiring nearly twice the wiring content. While an average ICE vehicle contains ~3.8 km of wiring weighing ~55 kg, an EV typically integrates ~4.2 km of wiring weighing ~68 kg, with around 13 kg dedicated to high-voltage wiring. With an estimated 395 million electric vehicles (BEV + Hybrid) expected to hit the roads between 2024 and 2030, the demand for high-voltage wires and cables is also set to rise.

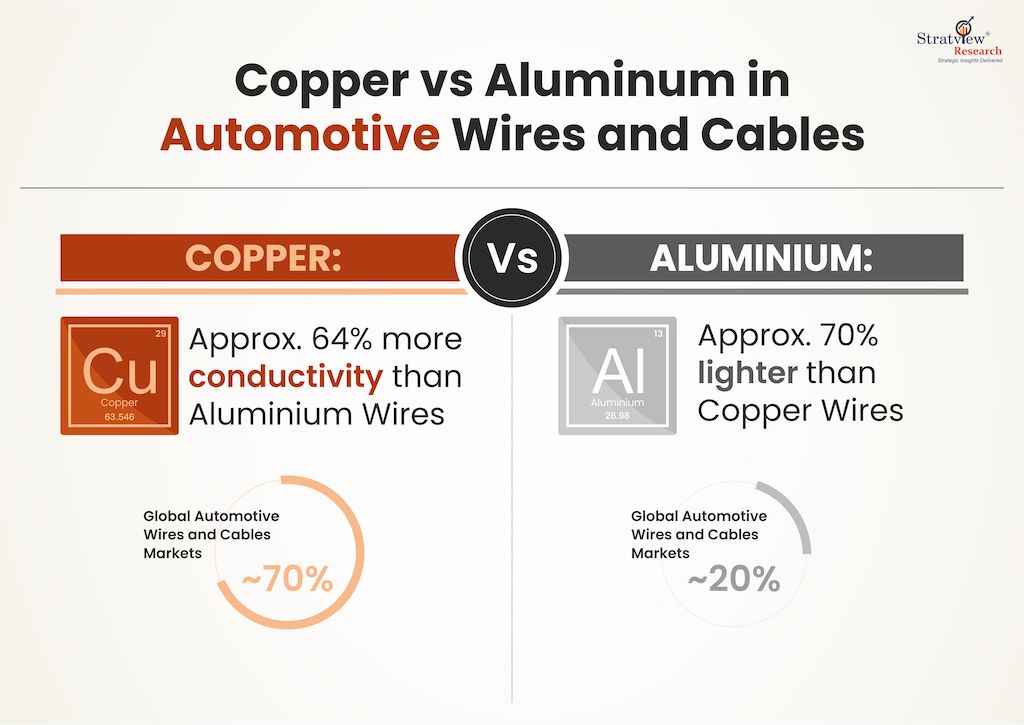

Material Choices – Copper Leads, Aluminum Follows:

Wires and cables are usually manufactured from a range of materials – copper being the top-notch choice to power the entire automotive wiring. Copper’s high conductivity makes it the ideal material not just for high-voltage applications but also for high-speed data transmission in vision systems and sensors, further cementing its role in modern vehicle architecture. An average ICE vehicle contains approximately 23 kg of copper, while an EV comparatively requires nearly three to four times more since they require copper in a number of things – a majority of them being their wiring looms, winding wire (motors), energy storage (foil and busbars in batteries) and power cables. Copper wires constitute nearly 70% of the total automotive wires and cables market globally.

On the other hand, there is a significant demand for aluminum as well. While the benefits of copper remain unmatched, aluminum’s lighter weight (70% lighter than copper) and lower cost make it the second most used material in automotive wiring, with around 20% market share. It directly reduces the overall weight of a vehicle, contributing to improved fuel efficiency. This makes it the key component in the automotive industry’s push for lightweighting.

The growing demand for alternative materials like aluminum might result in a short decline in copper usage per vehicle. According to Benchmark Mineral Intelligence, the average copper intensity per vehicle is expected to decline by almost 38 kg in coming years (from 99 kg in 2015 to 62 kg by 2030). Despite this, copper’s significantly higher conductivity – about 64% better than aluminum – means it will likely remain the market leader, as efficient conduction is simply non-negotiable in most applications, if not all.

Leaders in the Market:

The Asia-Pacific region is witnessing remarkable economic growth with soaring automotive production. In 2023, China’s automotive wire sales reached approximately US$ 18 billion, a figure larger than the combined sales of the next four major markets – Germany, Japan, India, and the USA. Interestingly, China holds about ~30% of the global automotive wires and cables market, making the APAC region the market leader with >55% of the market share. This is followed by Europe with ~21% market share, followed by North America with ~17% market share and the rest of the world holding the remaining share.

The Road Ahead:

Fuel efficiency is essential in the mobility industry. Notably, even a small weight reduction of around 50 kg in a passenger car can result in a 2% improvement in fuel economy. As a result, OEMs are always on the lookout for ways to reduce weight. Take a look at Tesla’s case – Tesla’s Model S has a total of 3 km of wiring. Astonishingly, in its newer Model 3, Tesla has been able to cut this down to just ~1.5 km. This presents a challenge to the industry to bring lighter and more reliable wiring solutions to the OEMs’ table.

Despite the challenge, wires and cables remain indispensable for most of their applications in the automotive industry. The market is undergoing significant transformations driven by the increasing electrification and automation of vehicles, and the market is expected to grow with a CAGR of 5.3% and hit around USD 78 billion by 2030, sprinting parallel to the growth in the global automotive industry.